library("RJDemetra")

# the input series has to be a Time Series (TS) object

# specification RSAfull including pre-treatment

model_sa_v2 <- tramoseats(raw_series, spec = "RSAfull")SA: Seats Decomposition

In this chapter

This chapter focuses on practical implementation of a Seats decomposition using the graphical user interface GUI and R using R packages in version 2.x and 3.x. More explanations on Seats algorithm can be found here.

In recent years Seats has been tailored in JDemetra+ to handle high-frequency (infra-monthly) data, which is described here with more methodological details here.

The sections below will describe

specifications needed to run Seats

generated output

Context

Seats is the second (decomposition) step in a seasonal adjustment processing with Tramo-Seats, once a pre-treatment with Tramo has been performed. Seats is an ARIMA Model Based (AMB) algorithm and will decompose the linearized series using the ARIMA model fit in Tramo.

Tools for Seats decomposition

| Algorithm | Access in GUI | Access in R (v2) | Access in R v3 |

|---|---|---|---|

| Tramo-Seats | ✔️ | RJDemetra | rjd3tramoseats |

| Tramo only | ✔️ | RJDemetra | rjd3tramoseats |

Available frequencies in version 2 and version 3

| Version | GUI and R |

|---|---|

| v 2.x | \(p=12, 6, 4, 2\) |

| v 3.x | \(p=12, 6, 4, 3, 2\) |

Seats Decomposition

Seats algorithm will decompose the linearized series, in level or in logarithm, using the ARIMA model fitted by Tramo in the pre-treatment phase. {#a-sa-seats-q-start}

Quick Launch

Default specifications

The default specifications for Seats must be chosen at the starting of the SA processing. Starting point for Tramo-Seats, detailed here

Using GUI

With a workspace open, an SAProcessing created and open data provider:

choose a default specification (link)

drop your data and press green arrow (link)

In R

In version 2 using RJDemetra

Full documentation of ‘RJDemetra::tramoseats’ function can be found here

The model_sa_v2 R object (list of lists) contains all parameters and results. Its structure is detailed here. It can be printed giving access to selected parameters, series and diagnostics.

print(model_sa_v2)In version 3 using rjd3tramoseats

library("rjd3tramoseats")

model_sa_v3 <- tramoseats(raw_series, spec = "RSAfull")

# the input series has to be a Time Series (TS) objectFull documentation of ‘rjd3tramoseats::tramoseats’ function can be found here.

The model_sa_v3 R object (list of lists) contains all parameters and results. Its structure is detailed here.

It can be printed giving access to selected parameters, series and diagnostics.

print(model_sa_v3)Retrieve Series

This section outlines how to retrieve the different kinds of output series from GUI or in R.

final components (including reallocation of pre-adjustment effects)

components in level

components in level or log

Stochastic series

Decomposition of the linearized series or of its logarithm (in case of a multiplicative model)

y_lin is split into components: t_lin, s_lin, i_lin

suffixes: - _f stands for forecast - _e stands for - _ef stands for

Display in GUI

NODE Decomposition>Stochastic series - Table with series and its standard error image

- Plot of Trend with confidence interval image

- Plot of Seasonal component with confidence interval image

Retrieve from GUI

Generating output from GUI (link) or from Cruncher (link), stochastic series, their standard errors, forecasts and forecasts errors can be accessed with the following names

| Series Name | Meaning |

|---|---|

| decomposition.y_lin | |

| decomposition.y_lin_f | |

| decomposition.y_lin_ef | |

| decomposition.t_lin | |

| decomposition.t_lin_f | |

| decomposition.t_lin_e | |

| decomposition.t_lin_f | |

| decomposition.sa_lin | |

| decomposition.sa_lin_f | |

| decomposition.sa_lin_e | |

| decomposition.sa_lin_ef | |

| decomposition.s_lin | |

| decomposition.s_lin_f | |

| decomposition.s_lin_e | |

| decomposition.s_lin_ef | |

| decomposition.i_lin | |

| decomposition.i_lin_f | |

| decomposition.i_lin_e | |

| decomposition.i_lin_ef |

Retrieve in R

In version 2

library("RJDemetra")

# list of additional output objects

user_defined_variables("Tramo-Seats")

# specify additional objects in estimation

m <- tramoseats(

series = y,

spec = "RSAfull",

userdefined = c(

"decomposition.y_lin", "ycal",

"variancedecomposition.seasonality"

)

)

# retrieve objects

m$user_defined$decomposition.y_lin

m$user_defined$ycal

m$user_defined$variancedecomposition.seasonalityIn version 3

library("rjd3tramoseats")

# list of additional output objects

userdefined_variables_tramoseats("tramoseats")

# specify additional objects in estimation

m <- tramoseats(

ts = y,

spec = "RSAfull",

userdefined = c(

"decomposition.y_lin", "ycal",

"variancedecomposition.seasonality"

)

)

# retrieve objects

m$user_defined$decomposition.y_lin

m$user_defined$ycal

m$user_defined$variancedecomposition.seasonalityComponents (Level)

Decomposition of the linearized series, back to level in case of a multiplicative model.

y_lin is split into components: t_lin, s_lin, i_lin

suffixes: - _f stands for forecast - _e stands for - _ef stands for

Displayed in GUI

NODE Decomposition>Components - Table with series and its standard error image

Retrieve from GUI

Generating output from GUI (link) or from Cruncher (link), component series, their standard errors, forecasts and forecasts errors can be accessed with the following names

| Series Name | Meaning |

|---|---|

| decomposition.y_cmp | |

| decomposition.y_cmp_f | |

| decomposition.y_cmp_ef | |

| decomposition.t_cmp | |

| decomposition.t_cmp_f | |

| decomposition.t_cmp_e | |

| decomposition.t_cmp_f | |

| decomposition.sa_cmp | |

| decomposition.sa_cmp_f | |

| decomposition.sa_cmp_e | |

| decomposition.sa_cmp_ef | |

| decomposition.s_cmp | |

| decomposition.s_cmp_f | |

| decomposition.s_cmp_e | |

| decomposition.s_cmp_ef | |

| decomposition.i_cmp | |

| decomposition.i_cmp_f | |

| decomposition.i_cmp_e | |

| decomposition.i_cmp_ef |

Retrieve in R

Same procedure as for stochastic series.

Bias correction

to be added

Final series

| Series | Final Seats components | Final Results | Reallocation of pre-adjustment effects |

|---|---|---|---|

| Raw series (forecasts) | y (y_f) | ||

| Linearized series | none | ||

| Final seasonal component | s (s_f) | ||

| Final trend | t (t_f) | ||

| Final irregular | i (i_f) | ||

| Calendar component | |||

| Seasonal without calendar |

(to be added: reallocation of outliers effects)

Display in GUI

Final results are displayed for each series in the NODE MAIN>Table

Forecasts are glued at the end it italic

Retrieve from GUI

Generating output from GUI (link) or from Cruncher (link), component series, their standard errors, forecasts and forecasts errors can be accessed with the following names

| Series Name | Meaning |

|---|---|

| y | |

| y_f | |

| t | |

| t_f | |

| sa | |

| sa_f | |

| s | |

| s_f | |

| i | |

| i_f |

Retrieve in R

In version 2

library("RJDemetra")

sa_model <- RJDemetra::tramoseats(y, "RSAfull")

sa_model$final$series

sa_model$final$forecasts

# for additional results call user-defined output as explained aboveIn version 3

library("rjd3tramoseats")

sa_model <- tramoseats(y, spec = "RSAfull")

# final series can be accessed here

sa$result$final$sa

# for additional results call user-defined output as explained aboveRetrieve Diagnostics

- WK analysis

components final estimators

Error analysis autocorrelation of the errors (sa, trend) revisions of the errors

Growth rates

Model based tests

Significant seasonality

Stationary variance decomposition

Retrieve Final Parameters

Relevant if parameters not set manually, or any parameters automatically selected by the software without having a fixed default value. (The rest of the parameters is set in the specification) To manually set those parameters and see all the fixed default values see Specifications / parameters section

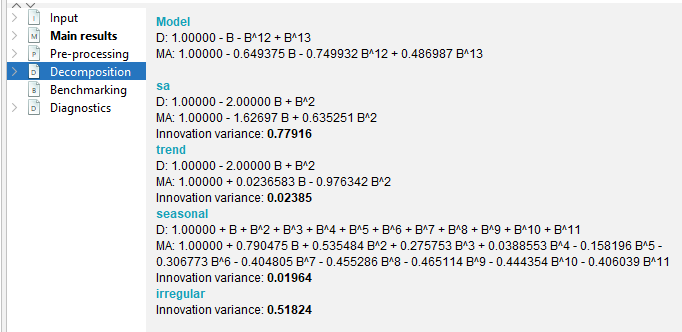

ARIMA Models for components

Display in GUI

Click on the Decomposition NODE

Retrieve from GUI

(add names for output and cruncher)

Display in R

(display or retrieve)

version 2

version 3

Other final parameters

Final parameters which can be fine-tuned be the user are described in User-defined specifications section below

Setting user-defined parameters

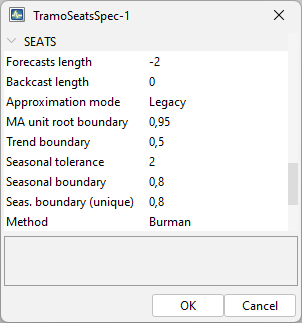

The section below explains how the user can fine-tune some Seats parameters, which are put in context in the corresponding method chapter.the default value is indicated in ().

- Prediction length

Forecast span used in the decomposition default: one year (-1) (years are set in negative values, positive values indicate number of periods)

- Approximation Mode

Modification type for inadmissible models None (default) Legacy Noisy

- MA unit root boundary

Modulus threshold for resetteing MA “near-unit” roots [0,1] default (0.95)

Trend Boundary Modulus threshold for assigning positive real AR Roots [0,1] default (0.5)

Seasonal Tolerance Degree threshold for assigning complex AR roots [0,10] default (2)

Seasonal Boundary (unique) Modulus threshold for assigning negative real AR roots [0,1] default (0.8)

Seasonal Boundary (unique) Same modulus threshold unique seasonal AR roots [0,1] default (0.8)

Method

Algorithm used for estimation of unobserved components

Burman (default)

KalmanSmoother

McEllroyMatrix

Seting parameters in GUI

In specification window corresponding to a given series:

Set in R

version 2 (RJDemetra)

tramoseats_spec(

spec = c("RSAfull", "RSA0", "RSA1", "RSA2", "RSA3", "RSA4", "RSA5"),

fcst.horizon = NA_integer_,

seats.predictionLength = NA_integer_,

seats.approx = c(NA_character_, "None", "Legacy", "Noisy"),

seats.trendBoundary = NA_integer_,

seats.seasdBoundary = NA_integer_,

seats.seasdBoundary1 = NA_integer_,

seats.seasTol = NA_integer_,

seats.maBoundary = NA_integer_,

seats.method = c(NA_character_, "Burman", "KalmanSmoother", "McElroyMatrix")

)in version 3 with {rjd3tramoseats} (to be added)