# Create a calendar with rjd3toolkit

# Define a national calendar

frenchCalendar <- national_calendar(days = list(

fixed_day(7, 14), # Bastille Day

fixed_day(5, 8, validity = list(start = "1982-05-08")), # Victory Day

special_day("NEWYEAR"),

special_day("CHRISTMAS"),

special_day("MAYDAY"),

special_day("EASTERMONDAY"),

special_day("ASCENSION"),

special_day("WHITMONDAY"),

special_day("ASSUMPTION"),

special_day("ALLSAINTSDAY"),

special_day("ARMISTICE")

))

# Generrate calendar regressors

q <- holidays(

calendar = frenchCalendar,

start = "1968-01-01",

length = length(df_daily$births),

type = "All",

nonworking = 7L

)

# Argument type = All : taking all holidays into account

# Argument type = Skip : taking into account only the holidays falling on a week daySA of high-frequency data

In this chapter

The sections below provide guidance on seasonal adjustment of infra-monthly, or high-frequency (HF), time-series data with JDemetra+ tailored algorithms.

Currently available topics:

description of HF data specificities

R functions for pre-treatment, extended X-11 and extended Seats

Up coming content:

Graphical User Interface 3.x functionalities for HF data

STL functions

State space framework

Data specificities

HF data often display multiple seasonal patterns with potentially non-integer periodicities which cannot be modeled with classical SA algorithms. JD+ provides tailored versions of these algorithms.

| Data | Day | Week | Month | Quarter | Year |

|---|---|---|---|---|---|

| quarterly | 4 | ||||

| monthly | 3 | 12 | |||

| weekly | 4.3481 | 13.0443 | 52.1775 | ||

| daily | 7 | 30.4368 | 91.3106 | 365.2425 | |

| hourly | 24 | 168 | 730.485 | 2191.4550 | 8765.82 |

Tailored algorithms in JDemetra+

| Col1 | Algorithm | GUI v 3.x | R package |

|---|---|---|---|

| Pre-treatment | Extended Airline Model | ✔️ | rjd3highfreq |

| Decomposition | Extended Seats Extended Airline Model | ✔️ | rjd3highfreq |

| Extended X-11 | ✔️ | rjd3x11plus | |

| Extended STL | ✖ | rjd3stl | |

| One-Step | SSF Framework | ✖ | rjd3sts |

SA algorithms extended for high-frequency data

All algorithms are available via an R package and will be available in GUI (in target v 3.x version)

Extended Airline estimation, reg-ARIMA like (

rjd3highfreqand GUI )Extended Airline Decomposition, Seats like (

rjd3highfreqand GUI )MX12+ (

rjd3x11plus, GUI upcoming)MSTL+ (

rjd3stland in GUI)MSTS (

rjd3sts, GUI upcoming)

Data frequencies and seasonal patterns

In the Graphical User Interface (display constraints)

Input data: daily, weekly

Seasonal patterns: weekly (\(p=7\)) or yearly (\(p=365.25\) or \(p=52.18\) )

In corresponding R packages:

no constraint on data input as no TS structure (numeric vector)

any seasonal patters, positive numbers

Unobserved Components

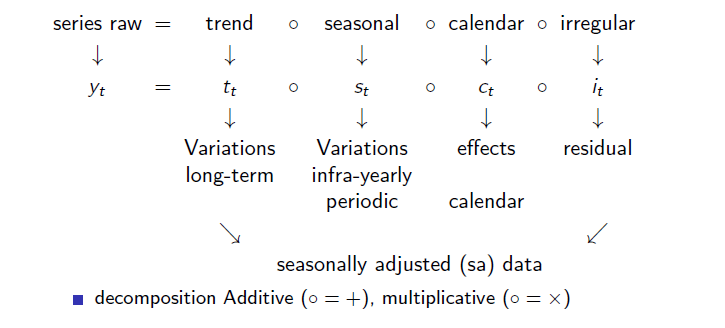

Raw series decomposition

Multiple seasonal patterns

HF data often contain multiple seasonal patterns. For example, daily economic time series often display strong infra-weekly and infra-yearly seasonality. An infra-monthly seasonal pattern may also be present, but its strength is usually less pronounced in practice. In theory, the full decomposition of the seasonal component in daily data is given by:

\[ S_{t}= S_{t,7} \circ S_{t,30.44} \circ S_{t,365.25} \]

The decomposition is done iteratively periodicity by periodicity starting with the smallest one (highest frequency) as:

highest frequencies usually display the biggest and most stable variations

cycles of highest frequencies can mix up with lower ones

Identifying seasonal patterns

JDemetra+ provides the Canova-Hansen test in the rjd3toolkit package.

Pre-adjustment

In classical X-13-ARIMA and Tramo-Seats, a pre-adjustment step is performed to remove deterministic effects, such as outliers and calendar effects, with a Reg-ARIMA model. In the extended version for HF data, it is also the case with an extended Airline model.

A general Reg-ARIMA model is written as follows:

\[ \left(Y_t - \sum {\alpha_i}X_{it}\right) \sim ARIMA(p,d,q)(P,D,Q) \]

These models contain seasonal backshift operators \(B^{s}(y_t)=y_{t-s}\). Here \(s\) can be non-integer. JDemetra+ will rely on a modified version of a frequently used ARIMA model: the “Airline” model:

\[ (1-B)(1-B^{s})y_t=(1-\theta_1 B)(1-\theta_2 B^{s}) \epsilon_t \text{~~~~} \epsilon_t \sim \text{NID}(0,\sigma^2_{\epsilon}) \]

For HF data, the potentially non-integer periodicity \(s\) will be written: \(s=s' + \alpha\), with \(\alpha \in [0,1)\) (for example \(52.18 = 52 +0.18\) is the yearly periodicity for weekly data)

Taylor series development around \(1\) of \(f(x)=x^\alpha\)

\[ \begin{array}{lll} x^\alpha &=& 1 + \alpha (x-1) + \frac{\alpha (\alpha+1)}{2!} (x-1)^2 + \frac{\alpha (\alpha+1) (\alpha+2)}{3!} (x-1)^3 +\cdots \\ B^\alpha &\cong& (1 - \alpha)+ \alpha B \end{array} \]

Approximation of \(B^{s+\alpha}\) in an extended Airline model

\[ \begin{array}{lll} B^{s+\alpha} &\cong& (1 - \alpha)B^s+ \alpha B^{s+1} \end{array} \]

Example for a daily series displaying infra-weekly (\(p_{1}=7\)) and infra-yearly (\(p_{2}=365.25\)) seasonality:

\[ (1-B)(1-B^{7})(1-B^{365.25)}(Y_t - \sum {\alpha_i}X_{it})=(1-\theta_1 B)(1-\theta_2 B^{7})(1-\theta_3 B^{365.25}) \epsilon_t \]

\[ \epsilon_t \overset{iid}{\sim} \text{N}(0,\sigma^2_{\epsilon}) \]

with

\[ 1 - B^{365.25} = 1 - (0.75B^{365} + 0.25B^{366}) \]

Calendar correction

Calendar regressors can be defined with the rjd3toolkit package and added to pre-treatment function as a matrix.

Outliers and intervention variables

Outliers detection is available in the pre-treatment function. Detected outliers are AO, LS and WO. Critical value can be computed by the algorithm or user-defined.

Linearization

Example using rjd3highfreq::fractionalAirlineEstimation function:

pre_adjustment <- rjd3highfreq::fractionalAirlineEstimation(y_raw,

x = q, # q = daily calendar regressors

periods = c(7, 365.25),

ndiff = 2, ar = FALSE, mean = FALSE,

outliers = c("ao", "ls", "wo"),

criticalValue = 0, # computed in the algorithm

precision = 1e-9, approximateHessian = TRUE

)“pre_adjustment” R object is a list of lists in which the user can retrieve input series, parameters and output series. For more details see chapter on R packages and rjd3highfreq help pages R, where all parameters are listed.

Decomposition

Extended X-11

X-11 is the decomposition module of X-13-ARIMA, the linearized series from the pre-adjustment step is split into seasonal (\(S\)), trend (\(T\)) and irregular (\(I\)) components. In case of multiple periodicities the decomposition is done periodicity by periodicity starting with the smallest one. Global structure of the iterations is the same as in “classical” X-11 but modifications were introduced for tackling non-integer periodicities. They rely on the Taylor approximation for the seasonal backshift operator:

\[ \begin{array}{lll} B^{s+\alpha} &\cong& (1 - \alpha)B^s+ \alpha B^{s+1} \end{array} \]

Modification of the first trend filter for removing seasonality

The first trend estimation is thanks to a generalization of the centred and symmetrical moving averages with an order equal to the periodicity \(p\).

filter length \(l\): smallest odd integer greater than \(p\)

examples: \(p=7 \rightarrow l=7\), \(p=12 \rightarrow l=13\), \(p=365.25 \rightarrow l=367\), \(p=52.18 \rightarrow l=53\)

central coefficients \(1/p\) (1/12,1/7, 1/365.25)

end-point coefficients \(\mathbb{I} \{\text{$E(p)$ even}\} +(p-E(p)) /2p\)

example for \(p=12\): (\(1/12\) and \(1/24\)) (we fall back on \(M_{2\times12}\) of the monthly case

example for \(p=365.25\): (\(1/365.25\) and \(0.25/(2*365.25)\))

Modification of seasonality extraction filters

Computation is done on a given period

Example \(M_{3\times3}\)

\[ M_{3\times3}X = \frac{1}{9}(X_{t-2p})+\frac{2}{9}(X_{t-p})+\frac{3}{9}(X_{t})+\frac{2}{9}(X_{t+p})+\frac{1}{9}(X_{t+2p}) \]

if \(p\) integer: no changes needed

if \(p\) non-integer: Taylor approximation of the backshift operator

Modification of final trend estimation filter

As seasonality has been removed in the first step, there is no non-integer periodicity issue in the final trend estimation, but extended X-11 offers additional features vs classic X-11, in which final trend is estimated with Henderson filters and Musgrave asymmetrical surrogates. In extended X-11, a generalization of this method with local polynomial approximation is available.

Example of decomposition

Here the raw series is daily and displays two periodicities \(p=7\) and \(p=365.25\)

# extraction of day-of-the-week pattern (dow)

x11.dow <- rjd3x11plus::x11plus(y_linearized,

period = 7, # DOW pattern

mul = TRUE,

trend.horizon = 9, # 1/2 Filter length : not too long vs p

trend.degree = 3, # Polynomial degree

trend.kernel = "Henderson", # Kernel function

trend.asymmetric = "CutAndNormalize", # Truncation method

seas.s0 = "S3X9", seas.s1 = "S3X9", # Seasonal filters

extreme.lsig = 1.5, extreme.usig = 2.5

) # Sigma-limits

# extraction of day-of-the-week pattern (doy)

x11.doy <- rjd3x11plus::x11plus(x11.dow$decomposition$sa, # previous sa

period = 365.2425, # DOY pattern

mul = TRUE,

trend.horizon = 371, # 1/2 final filter length

trend.degree = 3,

trend.kernel = "Henderson",

trend.asymmetric = "CutAndNormalize",

seas.s0 = "S3X15", seas.s1 = "S3X5",

extreme.lsig = 1.5, extreme.usig = 2.5

)ARIMA Model Based (AMB) Decomposition (Extended Seats)

Example

# extracting DOY pattern

amb.doy <- rjd3highfreq::fractionalAirlineDecomposition(

amb.dow$decomposition$sa, # DOW-adjusted linearised data

period = 365.2425, # DOY pattern

sn = FALSE, # Signal (SA)-noise decomposition

stde = FALSE, # Calculate standard deviations

nbcasts = 0, nfcasts = 0

) # Numbers of back- and forecastsSummary of the process

For the time being, seasonal adjustment processing in rjd3highfreq cannot be encompassed by one function like for lower frequency, e.g rjd3x13::x13(y_raw)

The user has to run the steps one by one, here is an example with \(p=7\) and \(p=365.25\)

computation of the linearized series \(Y_{lin}=ExtendedAirline(Y)\)

computation of the calendar corrected series \(Y_{cal}\)

computation of \(S_{7}\) by decomposition of the linearized series

computation of \(S_{365.25}\) by decomposition of the seasonally adjusted series with \(p=7\)

finally adjusted series \(sa_{final} = Y_{cal}/S_{7}/S_{365.25}\) (if multiplicative model)

STL decomposition

Not currently available. Under construction.

State Space framework

Not currently available. Under construction.

Quality assessment

Residual seasonality

JDemetra+ provides the Canova-Hansen test in rjd3toolkit package which allows to check for any remaining seasonal pattern in the final SA data.